UK property – time to sell? [2 of 2]

In this second instalment discussing the property investment pros and

cons for the UK, we will look more into the geopolitical and regulatory aspect

of the investment environment:

4) Warfaring disrupts business, causes capital

flight (to US/Asia)

The Ukraine

conflict is perhaps just the beginning of a reversal of human war cycles, as we

have bounced off the bottoms of more than one multi-millennial support lines in

the early 1990s:

|

Chart 17: conflict fatalities

may have hit long term bottoms and is turning up

|

As the peace dividend from the fall of the communist bloc in 1989 recede

into distant memory, could a new war hungry political set up be now in place to

drive conflicts going forward? Is the ascent of a new economic super-power

posing enough challenge to the existing order to lead to more hostilities?

With no ideological strive a la Cold War style (ie between communism and

capitalism), what might be the next bone of contention in conflicts? Could it

be domestic politics driven where international wars are mere diversions to

avoid power loss at home? Could the jaw dropping inflations in commodities

prices and food/energy shortages lead to resource wars?

We are now certainly in need of preparing, investment-wise, for a new

multi-polar world, and the upheavals the breakup of existing order ushers in.

One way to avoid being caught is definitely diversifying capital away from the

main players of such conflicts (eg Europe, or even parts of North Asia – e.g.

Japan).

UK, sadly sits too close to one of the main theatres of hostilities, and

taking profits on existing exposures may not seem too bad a thing to do!

Further, without the resource back up that some of our new target markets –

mostly commodities rich ones – are endowed with, UK is less well positioned to

weather the storm ahead:

|

Figure 1: Europe + Asia heavily

rely on energy imports (red) vs Americas + Oceania (yellow/green) net exporters of the same

|

5) Chasing out the rich – has the selling only just

begun?

The fervent confiscation of private property owned by individuals (see: indiscriminate seizures), who are not

state operators in the strict sense of the definition, could be a last straw

for any international investor considering the UK, as the current govt embarks

on a capital hostile regime only seen during wartimes. Seizing Russian wealth

without due process could be very dangerous for the country’s image as a safe

destination for investment, and harks back the harsh Japanese imprisonment

camps on USA mainland in WW2, not to mention what communist regimes did after

successful revolutions (eg in Russia in 1917, China in early 1950s).

Whilst the ‘totalitarian’ enemy are abstaining from similar tactics,

despite easily in position to confiscate western assets many times larger in

Russia, the fact that a now ideologically driven UK takes the lead within the

international community in asset forfeitures, without official declarations of

war (which must be authorised by parliament?), or due criminal court judgments,

really bodes ill for the future of London’s ability to attract investment.

Is it any wonder then that Superman KS Li (Hong Kong’s richest man) has

sold in Dec 2021 his London Broadgate investment after barely 4 years of

ownership for £1.25bn (a mere gain of 25%)? The fact that Cheung Kong often

leads the market in catching cycles has been legendary and was amply

illustrated by its HK$40.2bn sale of The Center in HK in 2017 which was mocked

at the time but today its buyers are licking the wounds of their 25+% losses.

Perhaps Mr Li has similar assessments on the deteriorating investment construct

that is UK? Not only that, CK has further ramped up its UK disposals by

flipping the much larger £15bn rump that is its power assets in March 2022 to

Macquarie and KKR (see here).

The investment and jobs that would otherwise have stayed in the UK in

the years ahead will now go for places less mob like, and more even handed,

like Dubai (see article here). As succinctly observed by another

commentator:

while many cheer the asset forfeiture of the evil Russian oligarchs,

other nations can and will use this new tactic of war in the future. ... How

could anyone feel safe investing in a Western nation if their assets will not

be protected?

Western governments have exposed themselves throughout this pandemic,

especially by letting us0 know they are not above coercion and silencing free

speech [eg curfew in Australia, bank acc seizure in Canada, big tech cancelling

of dissenting medical evidence]. The wealthy citizens are always the

first to flee when a city or nation is failing.

this will totally destroy the world economy as we know it. Foreign investment

in Russia will be seized, and the prospect of this migrating to China is

extremely high. A line has been crossed. You do not go after the assets of

private individuals claiming they are holding personal money for Putin. That

would be akin to saying someone was holding money for any politician simply

because they live under that leader’s rule.

This is a symptom of a major trend shift, and could mean a structural

loss for most of the traditional Western cities in their ability to attract

wealth in future from the Arabs, Chinese, Indians, and of course Russians…

Just to show how significant foreign capital is to the London market,

see how much they have multiplied over the 11 years to 2021:

|

Chart 18: Land Registry titles with individual

overseas owners – London a magnet for foreign capital

|

The 100s of thousands of property owners that felt UK was a safe place

to park money may now have doubts and start heading for the exits, especially

when the hostile political sentiment towards foreign owners continues to

escalate (e.g. in the fashion shown in Figure 2). Capital has no

loyalty, and will head where it is treated best.

|

Figure 2:

UK no longer a safe haven for foreign capital?

|

We suspect that as China sides with the opposite side of the UK

political narrative in this Ukraine conflict, it could be sooner rather than

later that Chinese money (eg including investors based out of HK) would also be

targeted for sanction/confiscation in this new norm of attack on private property.

What if Taiwan becomes the next geopolitical hotspot? Will it be too late to

pull out then? May be this is what Mr Li saw that prompted his disposal of UK

assets?

6) Regulations Overload is becoming unbearable –

for property investors

The assault of regulations on property ownership has been quite relenting

in the past decade, as we have outlined in detail before here. But this has not

stopped since, as the multiplying demands for compliance keep mounting,

examples include:

a) Property selling

now requires AML declarations, what red tape rationale is this? Below is

a form from our property agents:

|

Figure 3:

onerous form filling and reluctant law enforcement is now daily chore for

landlords

|

b) Our accountants wrote to us below as they are no longer able to

pretend compliance costs are negligible and will charge extra for

sharing the burden:

You will note that the letter includes reference to a Compliance

Surcharge which is a new item. You will undoubtedly be aware that all professional

firms face ever increasing regulation and scrutiny, requiring a significant

amount of additional staff and 3rd party resource to deal with matters such as:

• Anti Money-laundering legislation in onboarding and monitoring our clients

• Anti-bribery and Facilitation of Tax Evasion legislation

• Data Protection and GDPR requirements

• Increased regulatory compliance visits from professional bodies

• IT & Cyber Security

For some time now, we have been looking at the basis upon which we

charge our clients. It is no longer sustainable for us to absorb these

costs, which outstrip inflation in terms of growth.

…and apply a 2.5% Compliance Surcharge to our fees, as a direct

contribution to these costs.

c) Green costs – the new ambitious EPC requirements could set

back £13k-27k depending on the work needed for Grade D/E buildings, for details

see article here; Hamptons calculated that in the

North East, necessary upgrades would be equivalent to 83pc of the region’s

annual rental income, according to Telegraph;

d) Green costs for commercial property too – according to

Savills, proposed Department for Business, Energy and Industrial Strategy

(BEIS) framework would ensure that all non-domestic rented buildings achieve a

[even more stringent] minimum ‘B’ rating by 2030… 87% of the office stock has

an EPC rating of ‘C’ or below. This is why we have also started disposing our

commercial property in London on behalf of a client syndicate.

e) tax compliance becoming cumbersome – a prelude to much harsher

regime to come? Here is an example of a form that non-resident landlords have

to file to the HMRC, which no doubt will continue to lengthen going forward:

OVERSEAS

BUYERS OF UNITED KINGDOM PROPERTY

RESIDENCE INFORMATION

During

the Year:

Did

you have a home overseas? Y / N

How many days did you spend in the UK?

How many ties** to the UK did you have?

How many workdays did you spend in the UK?

How many workdays did you spend overseas?

** Ties to the UK are defined as follows (references to "tax year"

mean the year ended 5 April 2022) :

1 Your spouse / civil partner /

cohabitee or minor child was resident in the UK

2 You had accommodation available in

the UK for 91 days or more in the tax year

and you spent at least one night there

3 You worked (for 3 hours or more) in

the UK on 40 or more days in the tax year

4 You spent more than 90 days in the

UK in either of the previous 2 tax years

5 You spent more

"midnights" in the UK than in any other country

This body of

complex requirements sets a costly trap for anyone who enjoys the English

summer too much, or having sent kids to study there, not to mention those going

for business purposes…

7) Demographics less bullish

Post-Brexit, UK's

population growth should significantly slow, meaning lower pressures on the

otherwise very tight housing supply (Chart 19), with the impact of EU

citizens returning home a yet to be quantified negative factor:

|

Chart 19: very tight supplies

in UK may unexpectedly ease

|

Further, lockdowns also repelled a lot of international visitors

(reduces demand for Airbnb / short stay), added to that student population

drops from China (geopolitics), there may be more unexpected release of stock

otherwise unavailable.

As a result of all

of the above, we believe the UK market will face much stronger headwinds going

forward, and better risk adjusted returns may be had in other jurisdictions. In

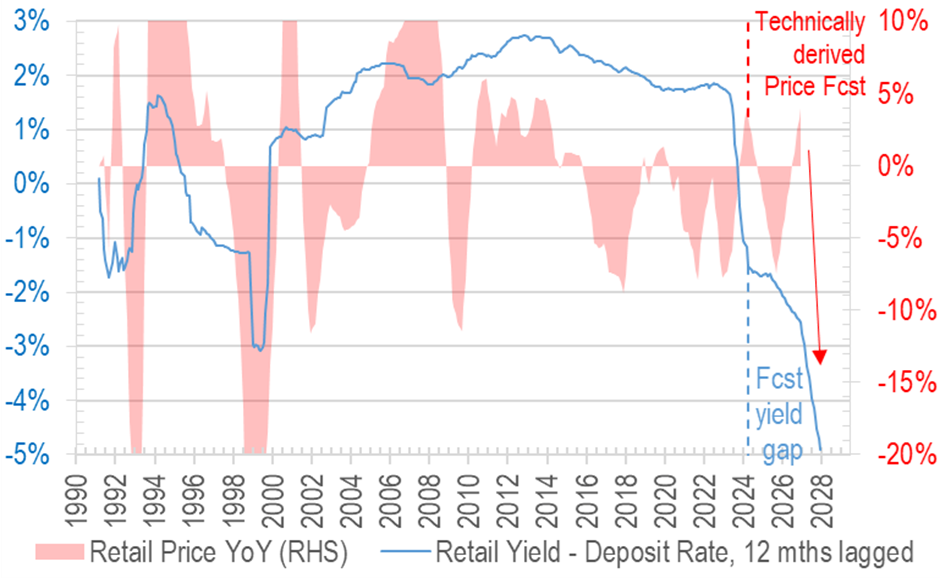

any case for the optimists, we present another technically derived upside forecast

as well, indicating possible rise of 14% (orange line) vs the most

bearish case of 21% price drop (blue line):

|

Chart 20: technical forecast

scenarios: -21% to +14% by end-25

|

Obviously, a lot of Hongkongers want to continue holding UK property for

asset allocation reasons rather than return maximising trades. For all B&MM

clients who feel action is needed as a result of this series of articles, we do

provide such services.

Where to go next?

'Go East' is probably the answer, if you compare the world reality of

barely two decades ago vs now (Figure 4); but if China risk is not your

cup of tea, then derivatives thereon (including commodities jurisdictions that

feed that growth) could well work... In the short term, however, capital

flights from Europe (or even Asia) could mean USA might be the ‘least dirty of

shirts’ in a world so screwed up with unparalleled amounts economic dislocations,

political divisions, and military risks.

|

Figure 4: Asia and commodities

are probably the lands of plenty in the long term

|

The author would like to thank Benson Kong Yu Chin

of The Hong Kong Polytechnic University for assisting in data collection,

analysis, and drafting of this article.