The combined favourable factors from capital flight due to the Ukraine/Middle East wars and HK's new national security legislation regime have massively pushed up investment demand for Singapore assets, thereby prompting headlines such as these of late:

>> Jack Ma's wife buys shophouses in ...Tanjong Pagar

for $37m (article 1);

>> Bridgewater

founder Ray Dalio joins

billionaires snapping up Singapore

‘shophouses’ (Article 3)

>> Singapore’s

shophouses — hotter than Fifth Avenue? (Article 4)

Whilst the first two

headlines might be interpreted as 'smart money' making early moves, the last

piece could be read as a sign of peaking market...

We continue to forecast

a new macro environment that is different from the good old days of near zero

interest rates and continued growth in global trade and productivity gains.

Instead, we believe the new reality is one of decoupling, deglobalisation, and

debt defaults, thanks to geopolitics and net zero / pandemic measures which not

only will drive further inflation, but will undermine high economic growth.

One of the consequences of the combined higher for longer inflation and debt default scenarios is rates staying high, or return to 90s highs, if not even 80s high levels:

Above SGP interbank

rates have already broken out of both the blue down trend as well as the lower

horizontal resistance over the past two years. If the worse outcome does pan

out as we feared, it might not be inconceivable to see rates hit 6.8% or thereabouts

in the next 2-3 years.

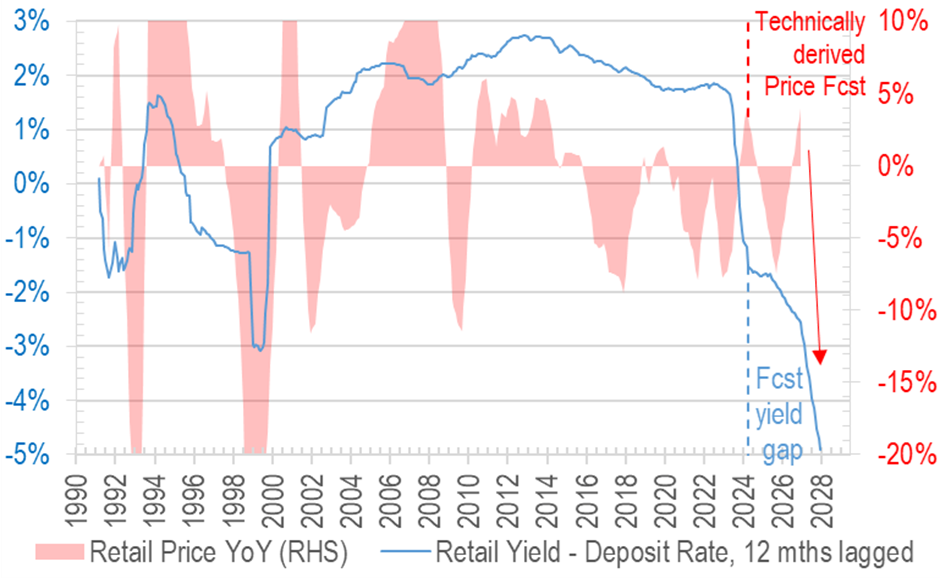

If Rent/Price moves can't match rate rises?

Using current trajectories in rent and price, we have modeled the near term yield increases, but sadly the rise in yields are not enough to offset the much more dramatic interest rate hikes, resulting in one of the more dramatic widening in retail yield discount vs deposit rates:

As a thought experiment,

we believe this is probably as bad as it gets, because we are not factoring in

the other capital flight which drove the rates higher - that from bonds.

Perhaps the initial crack in bond market (when yields go north of 6%) will be

negative for properties, but soon afterwards, the flight from bonds to real

assets (may unfold as early 2026) will completely reverse price performances to

the upside once more.

Based on this scenario,

we think not all investors need

to sell their safe haven assets (and indeed SGP shophouses are definitely safe haven in the

world we live in now), if

they can tolerate the price drops that happen before the final phase of the

upcoming yield expansion cycle...

In the meantime, the

very anaemic returns on retail property in SGP will continue to be a pain to

tolerate, especially for leveraged up owners:

Could SGP retail further

outshine HK in next few years?

The above wide gap

between yield and funding cost does indeed support our near term bearish

outlook on SGP retail assets, but if you look at the technicals vs HK retail

property, SGP retail has broken out of the green downtrend, and could be

hitting the blue channel top very soon (24% outperformance):

Should that level be

also breached, there could be even more upside to the top red resistance

(another 135% upside?).

Such a scenario probably

can only unfold if HK retail see another major leg down, and that could only be

driven by geopolitics rather than vanilla macro economics...

==================Article 1==================

Jack Ma’s Wife Buys Shophouses in Singapore’s Tanjong Pagar at Up to $37M

Beatrice Laforga | 2024/02/23

Despite stamp duties and

investigations, wealthy mainland investors are still banking on Singapore

properties, with the wife of the country’s best known tech tycoon having

purchased a row of shophouses in the Tanjong Pagar area last month for a

reported S$45 million to S$50 million ($33.5 million to $37.2 million).

==================Article 2==================

Shophouse sales surge and at higher prices in Q1 as high-net-worth investors return: Knight Frank

Samuel Oh | Fri, May 10,

2024 · 10:38 AM

In 2023, shophouse sales

came to 132 units worth S$1.2 billion. The number of units was 31 per cent

lower than the 191 units transacted in 2022 worth S$1.6 billion. Shophouse

sales have fallen from their peak in 2021, when a total of 254 units worth S$1.94

billion changed hands.

[...]

Knight Frank projects

the sales volume of shophouses to be between S$1.1 billion and S$1.2 billion

for the rest of 2024.

==================Article 3==================

Bridgewater founder Ray Dalio joins billionaires snapping up Singapore ‘shophouses’

Investor’s family office

bought two heritage properties for $19mn

Bridgewater Associates founder Ray Dalio’s family office has bought two multimillion-dollar “shophouses” in Singapore, as billionaires snap up the heritage properties in the city-state.

https://www.ft.com/content/9741784e-f69a-45cf-adf3-cc5b863c873f

==================Article 4==================

Singapore’s shophouses — hotter than Fifth Avenue?

Mercedes Ruehl / MAY 24

2024

Amid changing political

dynamics in South-East Asia, these colonial-era buildings have become some of

the world’s most expensive properties, home to Michelin stars and chichi

retailers — and a target for money launderers

https://www.ft.com/content/e1a53cb8-5bf0-408a-91a0-bcdd738c0f11