HK property is facing significant challenges, in the new reality of being increasingly viewed as 'another Chinese' city. Will this mean prices will fall more than its brethren in the north (or rise less if market turns up) henceforth? We look into a number of factors that influence the outcome of this interesting investment dynamic, perhaps starting with the bad news first: 1) Chinese outbound tourists bypassing HK (bad)? As more relaxations are introduced/restored for visa free entry to global destinations (right column in table below), PRC tourists may bypass HK even more and head for exotic climes directly:  This trend of disintermediation, is also manifesting with more overseas countries given visa exemptions for visiting China (left column above), a factor further compounded by increasing flights from gateway PRC airports to overseas cities, reducing the hub role HK has long come to enjoy. 2) Rising retail standard + cheap RMB => surging northbound HK shoppers (bad) As amply illustrated in article 1 below, increasingly sophisticated retail offerings in PRC cities, more spacious physical hardware, (sometimes) better services, and of course cheaper cost is now triggering a new phenomenon where HKers go spend weekends in SZ for leisure and even for grocery shopping. In office space alone, more companies may be tempted by the now Grade A spec but much more affordable occupation costs up north:

HK office costs are still 3x prime SZ equivalents, which coupled with cheaper labour, may entice increasing numbers of businesses to set up north of the border - especially if travelling on the High Speed Rail, one can be in Futian from Kowloon West in a matter of 14 minutes, on fares (book yours here) cheaper than the cost of a cup of Starbucks ... It is worth noting also that occupancy costs fell across the board in the China/HK markets in Q4 23, compared to mostly rises in other global cities - showing how weak the domestic economy was then, and why the Chinese govt had to pump prime to save the property sector in recent weeks. 3) PRC rate cuts vs Fed rate hikes (bad) We have long maintained that wars and deglobalisation will only worsen inflationary pressures, and that this would leave little to no scope for rate cuts by the Fed:

What's more, the still high real interest rates in China allows it ample further scope for credit easing - some 150bps vs US, and nearly 280bps vs UK):

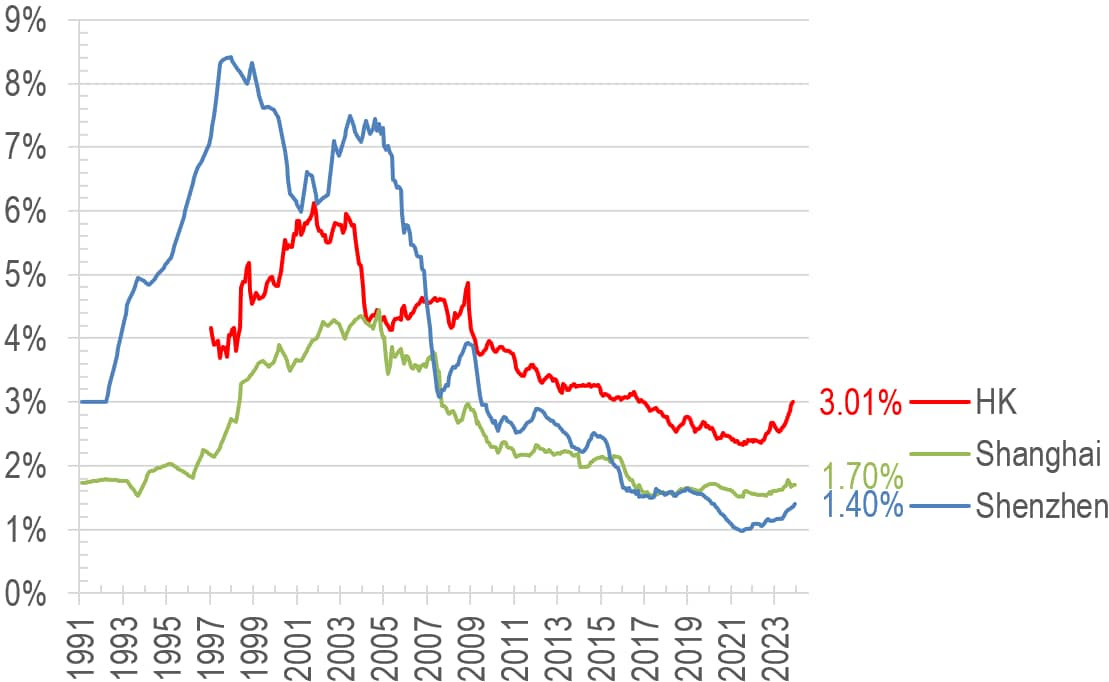

The conclusion of this rate trend divergence is best illustrated in the chart below:  Whenever HK rates hike less than PRC rates (green arrows pointing up, eg 1992, 2006), HK prices tend to rise much faster (red arrows up). The reverse is the case when HK rates rises more above PRC rates - which is where we are now - prices underperform SZ (eg 1996, 2013 to date). With the rate picture increasingly looking like HK rates staying high while China cuts further in the coming year (rightmost green arrow above), HK residential premium over SZ will likely shrink further in the coming two years. 4) Facilitating Southbound flows (good) The HK govt has been tapping into the rise in PRC wealth and talent by attracting them to settle in HK (article 2), but this is not radically different from some other immigration schemes already in place, and perhaps does not have as strong an impact as in earlier years. Similarly, attracting more southbound shoppers is nearing its potential (we already have 49 cities on easy travel arrangements, see article 4), and thus will unlikely result in any quantum leaps with further relaxations. 5) Higher SZ base good for higher HK too (good) As can be seen below, the premium in HK prices remain quite substantial over SZ for comparable luxury estates (Residence Bel Air in HK vs Seaworld Shuangxi Garden in SZ):  Whilst global comparison suggest that our current 120% premium may be too high - eg NYC Midtown is 50% premium over San Fran, and 63% premium over NYC Downtown - perhaps the shrinkage of the HK-SZ premium is largely done. Hopefully SZ price increases will do most of the catch up work rather than even deeper HK price drops... Looking forward, we think a combination of the two remains the most likely scenario; here the Price-to-income ratio trends suggest that SZ prices will improve by some 12% in the coming year or two whilst HK might see a larger 30% correction. For HK, the bulk of the improvement will have to come in price correction rather than income growth:  6) Yields already safer than many global cities (good) A saving grace for HK at least is that its real property yield is already quite 'reasonable' when viewed in the context of real property returns:  Above table is updated to December, showing that high inflationary pressures in places like Tokyo and London is destroying returns on rentals, whilst both SZ and HK sit reasonably happy in positive territory near the top of the pile. Generally high real return markets are more sustainable pricewise than -ve yielding ones. The higher nominal yield in HK (3%) also means that the higher interest rates here in the longer term will make for a healthier market when SZ's paltry 1.4%:

7) final technical look - SZ might do better medium term? On a long term technical perspective, SZ could continue to play catch up, but we await price action to give the next signal (either pierces the green support or breaks out of the blue resistance) before jumping into investment action. The answer might show itself by as early as mid-2024:

Given various headwinds in primarily geopolitics, perhaps investors are best to diversify into commodities and low conflict risk jurisdictions, exactly what we have been doing for the past 2-3 years... ==================Article 1================== Hong Kong vs Shenzhen: a day of food, drinks, sightseeing and leisure compared – how much cheaper can the mainland Chinese city be?The recent jump in people heading from Hong Kong to Shenzhen at the weekend suggests you can enjoy a lot more for much less in the mainland Chinese city... ==================Article 2================== Facilitation measures on two-way flow of high-end talents within the GBAThe Hong Kong Special Administrative Region Government and Mainland authorities have been exploring means to further facilitate the two-way flow of talents within the GBA, including “northbound” flow of non-Chinese Hong Kong residents.... https://www.info.gov.hk/gia/ ==================Article 3================== China cuts 5-year mortgage rate by record margin to aid property sectorThe People's Bank of China lowered the five-year rate to 3.95%, from 4.2%, marking the first reduction since last June... ==================Article 4================== 消息指中央同意擴大自由行來港 有議員料納入更多二三線城市現僅49個城市居民可自由行來港 部份省份無份原文網址: https://www.hk01.com/article/ English Google translate here. |

2024年2月23日星期五

Will HK fall more than SZ? 20240222

2023年8月4日星期五

Too much policy meddling trashes HK housing market 20230804

The SAR government’s launches of new housing policies have reached fever pitch in recent years: from Chief Executive Lee’s “Light Public Housing (LPH)” initiative from his 2022 Policy Address to this year’s resumption of “Private Sector Participation Scheme (PSPS)” that was abandoned in 2002, to the launch of Transitional Housing (TH)… All this begs the question of whether the government has a well laid plan for the long term, or just reacting furiously to show it is doing something to the rising home prices (which has now turned down)?

The stronger the price

rises, the bigger the temptation to interfere

Your correspondent has charted all the major public housing initiatives of

the past 60 years so as to demonstrate cause and effect, and to illustrate the motives

and timing of their launches. The result is clear: whenever major tinkering is made

to housing policies, it is often after sharp surges (see brown arrows in

Chart 1) or falls (green arrows) in home prices, for example:

a) The introduction

in 1977 of the Home Ownership Scheme (HOS) / PSPS (brown arrow A) was after

some 133% rise in home prices between 1971 and 1976 (see dotted line 1 on

the property price line); this was followed by

b) The Middle

Income Housing launch in 1980 coinciding with the end of another period of strong

price increases (dotted line 2), but then hastily cancelled in 1984 (green

arrow B) when the upcycle turned downwards after a final surge towards the

1981 peak (dotted line 3); likewise,

Chart 1: A timeline

of Hong Kong’s major public housing schemes changes

a) The continued

home price surge between 1985 and 1994, catalysed several further housing schemes

(Home Purchase Loan Scheme, Sandwich Class Housing, see brown arrows C-D),

as well as the final blast to mark the peak: the Tenants Purchase Scheme, Buy or

Rent Option, and even Mortgage Subsidy (arrow E), all launched before the

bubble burst in 1997 (dotted line 5);

d)

It was only after the 70% the collapse in home prices around the SARS bottom

that the government hurriedly withdrew as many as five housing interventions (green

arrow F)!

New up cycles, new intervention

temptations

Since the 2003 lows, the return of a housing upcycle (dotted lines 6+7)

yet again lured the authorities to launch several rounds of new measures in an attempt

to be seen as ‘doing something about affordability’, these included My Home Purchase

and the so called ‘practical but not extravagant’ new variety of HOS (brown arrows G+H)… go figure the multitude

of nuances in all these fancy layers of welfare!

Sadly for the mandarins in charge, the global zero interest rate environment

pushed property prices to even loftier heights, to finally reach a triple top in

2019-2022. This unacceptable situation had to be stopped, so in a flurry of new

initiatives, we saw Green Form HOS, White Form Secondary Market, followed by LPH/

Private Sales Subsidised Sale Flat Pilot Scheme/TH amongst others (brown arrow

I). All this illustrates is how confusing and short-sighted our housing policy

has been, with disappointing absence of logical philosophy on housing welfare provision.

Recent months, the increasing intensity and proliferation of initiatives

echoes the same panic last saw in the 1997 peak, presaging that another major top

may be in place for this cycle (cf arrow E vs arrow I): at the time of writing,

prices have fallen by 12% from the September 2021 highs. Your correspondent fears

that in another year or two, there may be a repeat of policy U turns saw at the

last major bottom (ie green arrow F vs arrow J)…

In order to illustrate the point on this predictable cycle, we plotted the

cause of policy actions (i.e. private home prices, see the blue line

in Chart 2) against the symptoms as expressed through the political

pressure (quantified by say the PRH waiting time, see green line), and then

the result being the number of government interventions (red line).

There is an eery correlation of the three:

The general pattern seems to be that the number

of public housing schemes (i.e. the frequency of market interventions) fluctuates

with the length of PRH waiting time; and the latter reflects of the swing between

greed and fear as property price fluctuates. The blue line in Chart 2,

being a lead indicator, suggests that as the decline in property prices continues,

average waiting time will also recede, to be followed by the phasing out of various

government schemes around 2025-7 (ie red line will turn down too).

What the above chart also suggests is that government

policies are always too little too late, what the various recent interventions/initiatives

are already 3-4 years too late, and the drop in home prices will mean that these

policies are yet again pro-cyclical, ie increasing price/demand volatility rather

than solving the root cause of the problem.

Simple is beautiful – learn

from Shenzhen?

Hong Kong’s housing welfare policy/administration has long been held hostage

by various vested interest groups, leading to endless proliferation of conflicting

policies which only complicate and confuse the people. But across the Shenzhen River,

our neighbour has a much simpler public housing set up, with only three layers and

minimal overlap with the private market. This enables much more focused welfare

delivery with less wastage – a real breath of fresh air indeed:

Even though housing policies in Shenzhen seem

to be driven strong property price moves just like in Hong Kong (see arrows a-c),

but changes to old schemes are accompanied by abolition of obsolete schemes that

no longer work. This is strong contrast to the dazzling array of overlapping complexities

that typify Hong Kong’s set up.

As a further example, Shenzhen plans to supply/allocate

80,000 welfare housing units (c. 4 million square metres in gross floor area) and

60,000 private units (c. 6 million square meters) in 2023. This translates to a

public : private unit and floor area ratio of 4:3 and 4:6 respectively; compared

with Hong Kong's overkill target ratio of 7:3, Shenzhen appears to have a freer

housing market!

Policy back to basics:

abolish HOS, reduce PRH

Since 1965, Hong Kong has launched a total of 18 public housing schemes,

of which 10 are still in force (Chart 1), but the housing problem has only

worsened. Not only has public housing policy been widely criticised for exacerbating

housing shortage, but has had the adverse effect of HOS breeding more of the “poor”

and the “lazy”; this is detrimental to social mobility, but also wastes vast amounts

of social and monetary resources.

In view of this quagmire, the government should radically reform as soon

as possible:

a) to make available

all HOS stock to the private market, this will immediately enlarge supply and can

rapidly bring property prices back to more affordable levels; and

b) limit scope

of PRH to the most needy, vulnerable group in society (rather than the current 35%

of all population!); by releasing land to the private leasing market, even the high

rents we see now stand a chance of moderating, thus lessening the pressure on the

government to engage in counterproductive market interference.

Chart 4: existing housing benefits a sore sight

of complete mess

If only the government would allow the invisible hand to allocate supply/demand

and prices in housing like so many other commodities are permitted to, then the

reason for the existence of such a mess and policy nightmare as shown in Chart

4 vanishes. When returned back to basics, the government’s role will shrink

to operating a basic safety net (red area in Chart 5) of physical

shelter provision, and perhaps as a transition into the private market, a limited

extension into rental vouchers but limited to say 10% of population. This way, even

the voucher recipients get freedom of choice in finding the right homes in the right

districts, and at the right prices according to the welfare beneficiary. Such an

elegant solution will also forever eliminate the endless expansion of bureaucracies,

sluggish liquidity/mobility in the housing market, and of course the constant exploitation

of an unfair welfare system – a blessing for Hong Kong from every angle one views.

A truly flexible, effective and fair proportion of housing provision by the

public sector should be as low as possible, and by no means the 7:3 ratio under

current policies (as indicated by the red arrow in Chart 6), by providing

low-level safety net physical housing (green arrow) coupled with monetary

subsidy for the next poorest group. If Hong Kong continues to imitate badly what

Singapore does for its own specific social political reasons, it will only be further

left in the dust by a younger, more dynamic neighbour in Shenzhen!

For a revision of some of your correspondent’s past analyses on Hong

Kong’s housing welfare, here are the links to recent publications for your

reference:

HK’s

Ever Ballooning Public Housing Addiction Cycle 11/2021 (Web, Blog, LinkedIn)

as well as some earlier writings in Chinese:

《居屋政策 好心做壞事 2014年7月》English Google translation (Web, Blog)

《公屋改革面面觀─租金偏離市場2014年9月》English Google translation (Web, Blog)

《公屋改革面面觀─結構性自我膨脹 2014年9月》English Google translation (Web, Blog)

《公屋改革面面觀─公屋「豪宅化」2014年10月》English Google translation (Blog)

The author would like to thank Alice Yurong Zeng from the Chinese University

of Hong Kong majoring in International Business and Chinese Enterprise for assisting

in data collection, analysis, and drafting this article.